Activity Based Costing Definition

Activity Based Costing (ABC) is a costing technique that is used to allocate indirect costs (overheads) to the products or service units in a more precious and logical manner. CIMA defines Activity Based Costing as a costing and monitoring approach that involves identifying consumption of resources and costing products, where the indirect costs are allocated to the product unit based on consumption estimates.

Activity Based Costing approach for costing a product is known as a rational approach compared to the traditional overhead allocation, where overheads are allocated based on direct labour hour or machine hour consumption. Unlike this traditional costing approach, Activity Based Costing system allocates overheads to the product item in two steps defined in a rational manner. First, the overheads are accumulated for each identical organizational activity that is identified as the actual reason for that cost may occur. Then, those costs are allocated only for the products that require those activities.

Activity Based Costing Activities

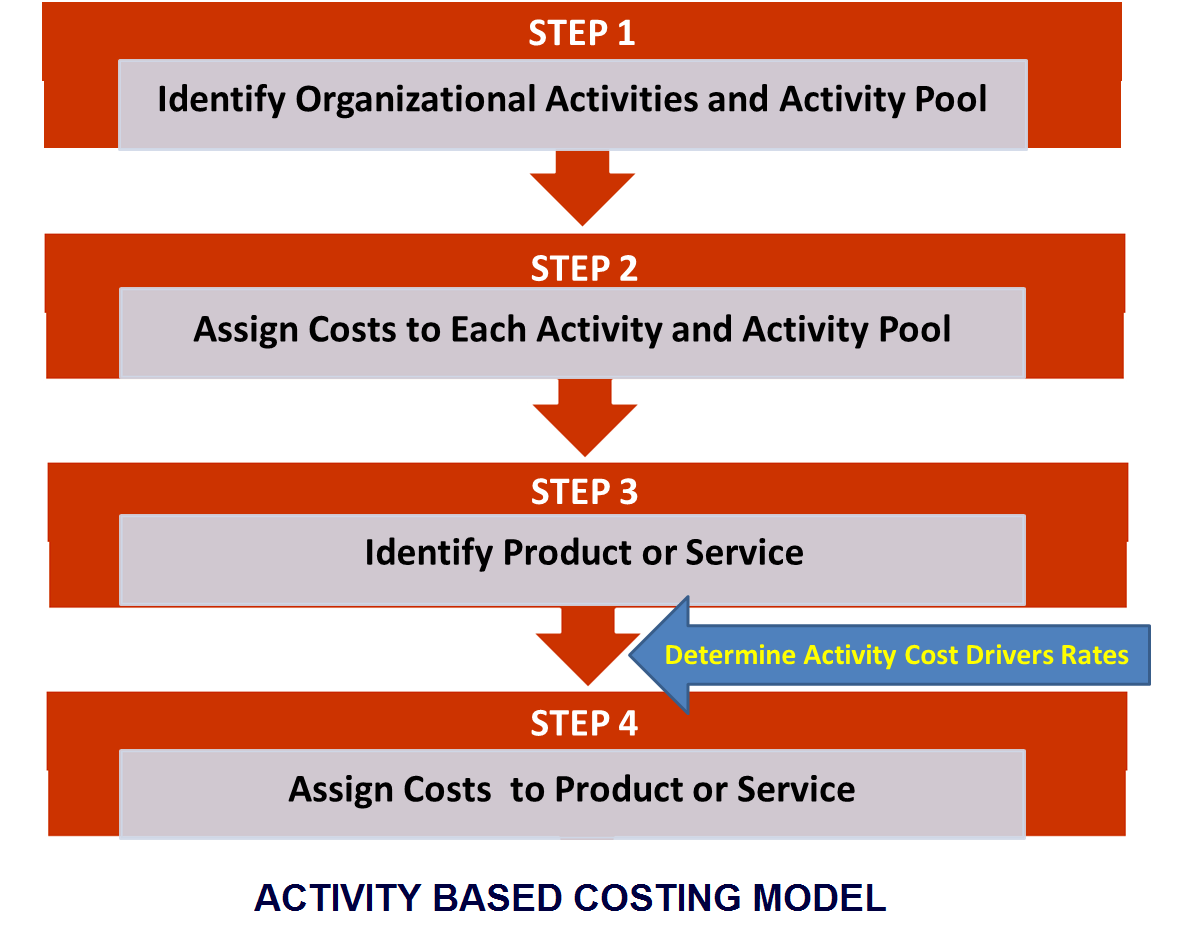

Activity Based Costing system involves four main activities.

1. Identification of organizational activities –Organization undertakes a detailed analysis and find out all the operating processes conducted by each responsibility centre.

2. Assigning costs to each activity – This step involves tracing costs into respective cost objects. Direct costs are traced directly to the output whereas indirect costs are assigned to each activity on the basis of respective cost drivers.

3. Identifying outputs – This may be a product or service.

4. Assigning costs traced for each activity to products – using appropriate cost drivers, pool of overhead costs are allocated to the output based on its consumption of such activities.

Dramatically increasing manufacturing overhead costs, not having a direct correlation between overhead cost and machine or labour hours, the diversified nature of the products produced by the companies and the consumer demand and mass scale production batches have resulted in increasing the importance of Activity Based Costing in the costing discipline.

Advantages of Activity Based Costing

• This method is identified as a more accurate costing approach for products and services where the calculation of cost per unit is more accurate compared to the traditional costing method. This aids in setting sales and pricing strategies as well.

• This method provides a concrete and rational understanding about each of the overhead cost element and the underlying causes for its occurrence

• Different cost elements used in manufacturing products such as value adding, and non-value adding costs are clearly visible under this method. This facilitates internal decision making.

• This method provides some links to the other management disciplines such as performance management, balanced scorecard and continuous improvement.

Disadvantages of Activity Based Costing | Limitations of Activity Based Costing

• This method involves a large amount of data about different activities and cost drivers. Therefore, this method is a time consuming and cost consuming approach.

• There are some costs that cannot be assigned to a specific activity within the organization (Ex- Chief Executive’s salary). Therefore, the accuracy of CPU calculated may not be assured.

• Activity Based Costing heavily focuses on attention to detail. Thus, this may affect the attention and control that the management has over the strategic goals of the organization.

How to Calculate Activity Based Costing

Photo By: Willie Hidelbach (CC BY-ND 2.0)

Leave a Reply